The Risk

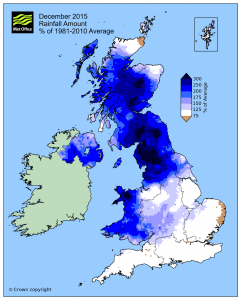

Last winter the UK experienced the second wettest December on record, and the warmest December since 1934, with average temperatures resting at around 8°C – about 4°C above the average.

But it is the extreme rainfall that has resulted in significant damage to properties across some parts of the UK, with around 16,000 homes and businesses in England flooded as a result of three major storms:

Storm Desmond: Hit in early December 2015. Cumbria was the most badly affected, experiencing a month’s rain (13.44 inches) in just one day. Rivers in Cumbria reached their highest levels ever.

Storm Eva: On Boxing Day 2015 many homes in Yorkshire and Lancashire were evacuated due to heavy flooding. Flood warnings were issued from Scotland to Wales.

At the end of December 2015, storms and gales hit throughout the West with more flooding in Scotland. One person is reported to have died as a result of Storm Frank.

Recent figures show that over 5.5 million homes in the UK are at risk of flooding – this is one in every five households. 2 million of these are classed as moderate risk or greater.

The Financial Cost

The Government has announced £200 million of additional investment to aid recovery from these winter floods.

Some of the hardest hit areas are flooded year after year, and it is costing our economy billions of pounds. Every flood generates thousands of insurance claims and the cost of these claims alone is adding up significantly:

- 2005: £272m

- 2007: £3.2bn

- 2009: £276m

- 2012: £594m

- 2013/2014: £451m

- 2015: £1.5bn (estimated)

However, despite this huge cost, these figures do not reflect the true financial impact of the floods.

Underinsured

Every flood requires a huge and costly cleanup operation, as well as repairs and upgrades to flood defences. Alongside the insurance claims, many home and business owners also have to foot the restoration costs themselves, due to inadequate cover.

The most recent floods in winter 2015 are anticipated to cost the insurance industry £1.5bn, with a further £1bn being paid out directly by home and business owners who are not adequately insured. A further bill for £2bn is estimated for flood defence repairs, and a review and development of the insurance sector (to limit the impact in the future) is costing around £500m.

Business Costs

Around 50% of insurance claims for the December 2015 floods are estimated to be from commercial businesses. Usually, this figure is between 10% and 30%, but as the floods hit many towns and cities, more businesses have been impacted.

There’s an estimated 185,000 commercial properties at risk of flooding in England and Wales, and the cost of flood damage can be so extensive that many wouldn’t be capable of recovery. The average cost of a flood to a business is around £28,000.

These losses extend further than just being closed for a few days. There are many ‘grey areas’ to commercial insurance cover, with loss of attraction and loss of market value typically not covered, not to mention the significant costs to absorb whilst the business is recovering, such as:

- Water damage can destroy the decor and even the structure of the premises, meaning a costly and drawn out refurb project – all whilst the business is losing day-to-day revenue caused by the downtime.

- The loss of stock alone for retail businesses can be difficult to recoup, but this is compounded by the loss of business assets, such as furniture, IT equipment and business records.

- The cost of keeping staff on retainer or continuing to pay their salary whilst the business is not earning revenue.

- Many businesses also risk losing their relationships with commercial partners if they can not continue to contribute to the supply and demand chain with their products or services.

Property Values

Home and business owners are suffering from a further financial burden as the property prices in flood risk areas are increasing at a significantly lower rate than those not in flood risk areas.

The most severely affected are those in the North where properties at risk of flooding (between 2005 and 2014) have increased in value half as fast as those at no risk.

In Yorkshire and Humber, this is most noticeable as the value of high-risk properties grew at 5.91%, when the value of no-risk properties grew at 16.29%.

Types of Flooding

There are different types of flood and the UK has been hit by all of them – each type impacts the flooded area in different ways. The level of damage and the recovery costs will depend on the type of water, the number and type of properties in the area, and the longevity of the flood.

Tidal Flooding: Flooding that occurs from sea or from tidal rivers. This type of flooding is usually sudden and extremely dangerous.

Surface water flooding from heavy or prolonged rainfall. Often exacerbated by flooded drainage systems that overflow.

Fluvial Flooding: Heavy rain and snowfall can exceed the capacity of rivers and watercourses, causing them to burst their banks, flooding the surrounding area.

After prolonged or extremely heavy rainfall, the ground can become so waterlogged it can no longer drain water away naturally. Often, the effects of groundwater flooding are worsened by concreting over large open areas, leaving nowhere for the rain to go.

Sewer Flooding: Sewer flooding can result from damage in the sewerage system, or the capacity of the system can simply be overwhelmed by heavy rain, flash flooding or groundwater flooding.